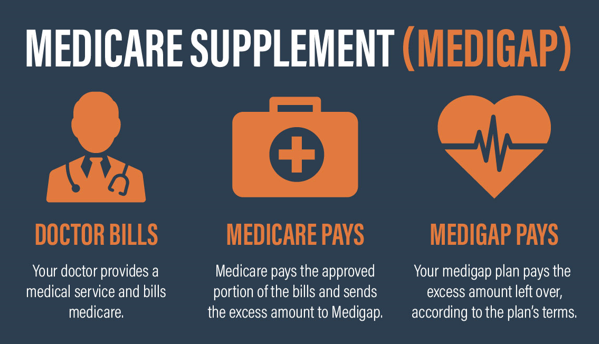

When you reach the age of 65, Medicare does not cover all of your medical bills. Part A of Medicare covers 80% of inpatient hospital and skilled nursing facility care, while Part B covers 80% of outpatient therapy and medically necessary supplies. You can acquire Medicare Supplement (Medigap) insurance from a commercial insurance firm to cover the 20% not covered by Medicare.

We analysed data on U.S. insurance companies that provide nationwide plans by the number of states in which they offer coverage, the number of types of plans they give, how they ranked in terms of financial health by agencies such as A.M. Best, and more to determine the best Medicare Supplement providers. Please keep reading to find out which vendors made our list.

Best Medicare Supplement Companies in 2023:

- Humana

- AARP by UnitedHealthcare

- Allstate Medicare Supplement (https://www.medisupps.com/medicare-supplement/allstate-medicare-supplement/)

- Mutual of Omaha

- Cigna

Selection of the Best Medicare Supplement Providers in 2023

To find the top Medicare Supplement providers for 2023, we assessed all insurance firms that sell plans across the country in the criteria:

- How many states do they give coverage in?

- The amount of Medigap plan options they provide

- Whether they expressly provide Part D (prescription medication) coverage.

- Whether they can give additional coverage beyond what federal requirements demand of Medigap insurance.

- M. Best financial health rankings (which influence how dependable an insurer is when it comes to paying claims)

- Consumer feedback on J.D. Power rankings

Its sole purpose is to provide broad descriptions of the companies and their reputations. The ZIP code and demographic information of the individual requesting insurance coverage must be considered to give reliable plan suggestions. It is suggested that you use Medicare.gov’s plan-finding tool or seek the advice of an independent, unbiased insurance agent.

What is a Medicare Supplement Plan (Medigap)?

Medicare Supplement, often Medigap, is a private insurance coverage acquired to pay for what Original Medicare (Parts A and B) does not cover. These supplementary coverage plans are only available with Original Medicare and do not apply to other private insurance policies, freestanding Medicare plans, or Medicare Advantage plans. Prescriptions are frequently excluded from Medigap plans, so you should consider registering in Medicare Part D, which explicitly covers prescription medications or a Medicare Advantage plan that includes drug coverage.

Medigap policies differ from Medicare Part C, often known as Medicare Advantage. When a Medicare Advantage plan can supplement Medicare Parts A and B, Medigap insurance only covers what Parts A and B do not.

Do You Qualify for Medicare Supplement?

To be qualified for a Medicare Supplement plans, you must be registered in Original Medicare Part A and Part B, but not in a Medicare Advantage plan. You have to be a member of one of the following groups:

- 65 years and older

- Under the age of 65 and getting disability benefits

- Under the age of 65 and suffering from amyotrophic lateral sclerosis (ALS)

- Under the age of 65 and suffering from end-stage renal disease (ESRD)

Companies may postpone coverage for a pre-existing illness for up to six months if you did not have creditable coverage (other health insurance) before enrolling in Medicare. Even if you delayed registration because you had group health insurance, your Medicare Supplement open enrollment period begins the month you join up for Medicare Part B insurance at the age of 65 or older. Even if your health condition changes, your Medigap coverage cannot be cancelled as long as you pay monthly. You can apply to purchase or switch insurance with Medigap coverage.

What Is the Cost of Medicare Supplement?

The cost of Medicare supplements varies according to the carrier and plan selected. According to Brandy Corujo, partner with Cornerstone Insurance Group in Seattle, not every insurer provides all policies. Individual insurance firms that sell Medigap policies choose their pricing. Companies in one of three ways determine premium pricing:

- Community-rated: Premiums remain constant regardless of age.

- Age-rated issue: The premiums are lower when insurance is obtained at a younger age. Premiums do not rise as you become older.

- Attained-age-rated: Your premium is determined by your age at purchase. Your premium rises as you become older.

Your location, gender, marital status, and lifestyle (such as whether or not you smoke) may all impact your premiums. Medigap plans are acquired from a private insurance company, and you pay a monthly payment to the company directly. Medigap plans can be acquired from any insurance company authorised to offer them in your state, although available policies and rates vary by state. Because Medigap insurance only covers one person, married couples must get separate policies.

Which of the Medicare Supplement Plans F, G, and N Is the Best?

Medicare Supplement Plans F, G, and N are the most popular Medigap plans in the United States, with the most significant enrollment rates. Their healthcare needs determine which one is ideal for the beneficiary.

Plan F is the most popular Medicare Supplement plan because it generally covers more out-of-pocket Medicare payments than any other Medigap plan type. Plan F covers Medicare deductibles, copays, and other fees connected with Medicare-covered treatments, allowing beneficiaries to avoid out-of-pocket spending. Plan F, on the other hand, is no longer available to any Medicare recipient who became eligible on or after January 1, 2020.

Due to these enrollment limits, Plan G is fast becoming the most popular Medicare Supplement plan type for new Medicare enrollees since it covers the greatest significant Medicare outlays of any Medigap plan available to all beneficiaries. Beneficiaries of Plan G must only pay their yearly Medicare Part B deductible, after which the plan covers 100% of all Medicare-covered medical expenditures.

Finally, Plan N is the third most common form of Medicare Supplement plan, supporting subscribers who want a wide variety of coverage. It covers 100% of Medicare Part B coinsurance payments, except $20 office visit copays and $50 ER visit copays. Beneficiaries must also pay the yearly Part B deductible. This arrangement keeps the plan’s cost relatively modest despite the danger of increased out-of-pocket spending, which is why people with fewer medical requirements choose it.

Conclusion

The optimal time to sign up for a Medicare Supplement plan is during your first Medigap Open Enrollment Period, which starts on the very beginning day of the month; you become 65 and are registered in Medicare Part B. This is the only time when insurance firms cannot refuse coverage based on your health status or medical condition. Attempting to enrol in a Medicare Supplement plan outside of this timeframe may result in penalty fines or rejection of coverage.